In many M&A transactions litigators become involved only after a dispute has arisen. However, a litigator’s experience in handling post-M&A disputes can give them an insight into the risks and common problems that arise in M&A transactions post-completion, and how these may be best mitigated at the contract drafting and management stage.

At Baker McKenzie our M&A disputes specialists work as a team with our corporate colleagues in order assist in managing and mitigating risk at both the drafting stage and post-completion. Here are ten of our top tips for minimising M&A risk.

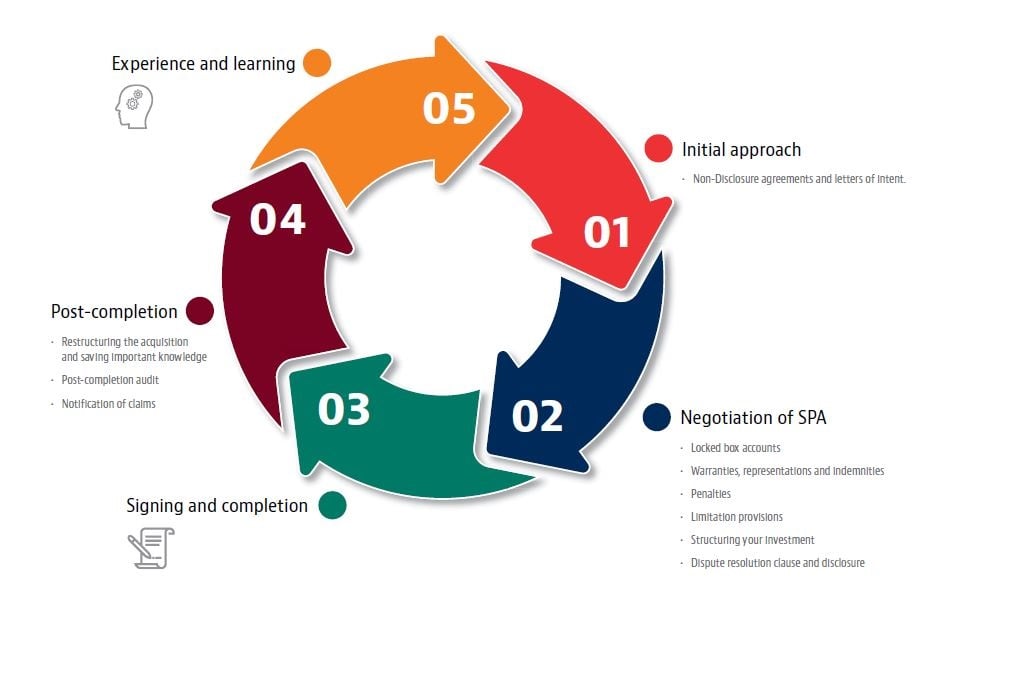

The M&A Lifecycle

Non-Disclosure agreements and letters of intent

Non-Disclosure agreements and letters of intent

Before parties start with detailed negotiations about a potential M&A transaction, they often agree on a Non-Disclosure Agreement (NDA) to ensure that confidential information will not be disclosed by the other party. Often the mere existence of negotiations will need to be treated as confidential. NDAs are sometimes contained in letters of intent (LOI) outlining the key terms of the proposed transaction. Though generally LOI are not intended by parties to be legally binding in all respects, often there are disputes regarding this and as to which provisions were intended to be binding. The possibility of the LOI creating a binding acquisition agreement becomes a significant risk factor if the LOI is not drafted properly.

![]() TEAM TIP:

TEAM TIP:

Parties should carefully define what constitutes confidential information and in which cases disclosure is nevertheless permitted (e.g. if disclosure is required by state authorities or statutory provisions). A potential buyer should avoid an NDA that might effectively amount to an non-compete obligation, although a seller will have a legitimate interest in ensuring that the potential buyer does not use the diligence exercise to solicit its key staff. Whilst the majority of the obligations will be on the bidder, bidders should also consider the extent of any protection they can legitimately request in light of any access to information and personnel they may provide during the transaction process. In a LOI parties should set out clearly what provisions are legally binding (such as exclusivity, confidentiality, non-solicitation, governing law and dispute resolution) and what provisions are not intended to be legally binding (such as the purchase obligation and the price).

Locked box accounts

Locked box accounts

Locked box accounts are proving increasingly popular and research suggests that they significantly reduce the risk of accounting related disputes compared with completion accounts. The clean break on completion, reduction of scope for dispute and the ability to focus on integration after completion are all benefits. However, the lack of postcompletion adjustments means the buyer assumes the economic risk before the target’s ownership is transferred. Any permitted value extraction (permitted leakage) from the target between the locked box date and closing therefore benefits the seller.

![]() TEAM TIP:

TEAM TIP:

If parties agree on the use of locked box accounts, they should define clearly which, if any, leakage is permitted. Once completion has taken place checks should be carried out immediately to ensure that no unpermitted leakage has taken place.

Warranties, representations and indemnities

Warranties, representations and indemnities

Common practice today is for sellers to avoid warranties also being given

as representations. Buyers should be aware of how this may impact the

calculation of damages under some governing laws and the sums that might

be recoverable. Framing warranties as also being representations provides

the option of a tortious claim which can sometimes lead to a higher damages recovery depending on the facts. This is especially the case where the buyer has over paid for the business in any event and is looking to recover value through damages by reference to the amount of its original outlay.

![]() TEAM TIP:

TEAM TIP:

If a buyer might be paying above the objective market value for a

business (e.g. because there are particular benefits specific to that buyer

(e.g. particular synergies)), the buyer may wish to argue that warranties

be repeated as representations. However, given current market practice

rejects the framing of warranties as representations, it is highly unlikely that

such an approach will be acceptable to a seller. Alternatively, therefore, the

buyer should carefully document the basis for valuing the target business

and ensure, in as far as practicable, that losses on that basis are within the

seller’s contemplation, which is most securely achieved by including the

valuation basis in the contract.

If such warranties or representations are limited by the seller’s knowledge,

the drafting of what constitutes knowledge can be critical to the scope of

the warranty/representation and the relevant risks and benefits to the seller

and buyer, respectively.

Similarly, care should be taken as to whether known potential issues are

dealt with by way of a warranty or indemnity. Typically, known issues will

be addressed by way of an indemnity, principally because: (a) standard deal

terms will mean that knowledge gleaned by a buyer from a formal disclosure

process will prevent a warranty claim in any event; and (b) there is legal

uncertainty as to the effect a buyer’s knowledge of an issue, obtained other

than through formal disclosure, has on its ability to claim damage, and the

quantum of those damages, for breach of a related warranty. Care, however, will need to be taken with drafting the indemnity in order to cover not just the cost to the target of rectifying or otherwise dealing with the issue, but the impact it has on the buyer’s valuation of, and price paid for, the target.

Penalties

Penalties

Often parties will seek to deter any breach by including a penalty provision should a breach occur. The concept of a penalty covers not just monetary sums which are referred to as such by name, but also other payment obligations, and obligations to repay a proportion of the consideration representing goodwill should there be a breach of the non-compete covenant or an obligation to transfer shares at some form of discounted price. Such penalty provisions can be effective in ensuring compliance with the terms of the SPA, but they can be found to be unenforceable as an illegitimate penalty. As such, significant care needs to be taken in the structuring and drafting of such clauses to ensure that they are strong enough to deter a potential contract breaker, but still remain enforceable.

![]() TEAM TIP:

TEAM TIP:

Where possible:

- Seek to draft any clause in a manner that makes the steps to be taken an independent primary obligation rather than a secondary obligation which only arises following a breach of contract.

- Set out the legitimate business interest that is sought to be protected by the clause.

- Ensure the consequences of any breach could not be considered to be extravagant,

exorbitant or unconscionable in light of the interest in performance and consider

adding an express statement in the SPA that, following legal advice, both parties

consider this to be the case. - Avoid a one size fits all clause or a penalty that is triggered by potentially different

breaches of varying significance. A clause that provides for the same consequences

whether the breach is significant or trivial is less likely to be enforceable. - Do not label the provision as a “penalty”.

Limitation provisions

Limitation provisions

The inclusion of financial limitations of liability (usually for the seller) is one of the main ways for a party to manage its liability risk. It allows both parties to know at the outset what the potential exposure and scope for recovery might be and to mitigate this risk accordingly (e.g. through insurance or an adjustment to the purchase price).

![]() TEAM TIP:

TEAM TIP:

The buyer should consider whether any known issue should be specifically excluded from any financial limitation of liability or be subject to its own separate cap. The parties to a transaction can also limit their risks by purchasing warranty insurance. If so, the parties cover the risk that a warranty is breached under an insurance contact and agree on a

limitation of liability of a nominal amount. If the transaction is structured this way, the insurer monitors the negotiations of the parties to properly assess the insured risks.

Structuring your investment

Structuring your investment

Where an acquisition is made overseas, the investment should be

structured to ensure not only favourable tax treatment but also to ensure

that the investment benefits from investor protections under a bilateral

investment treaty (BIT) or similar public international law instrument.

This may require the acquisition to be structured in a particular manner,

for example through an SPV based in a specific jurisdiction which has a

BIT with the country in which the target is located.

A BIT offers protections to investors against unlawful acts of the

host state. Such protections often include requiring the payment of

compensation in the event of expropriation, requiring the treatment of

the investor to be no less favourable than the treatment of nationals of

the host state or investors from other countries, and fair and equitable

treatment (including the right to procedural fairness, due process and

transparency, and freedom from coercion or harassment). BITs can be seen

as a free form of (limited) insurance against political interference in the

investment and should be considered for all overseas acquisitions.

![]() TEAM TIP:

TEAM TIP:

Buyers making an international acquisition should check if a BIT is in

place between the place of its own business and the target’s location.

If not, the acquisition should be structured, in conjunction with tax

structuring, in order to obtain the benefit of protections for the buyer’s

investment under at least one BIT. It should not be assumed that all

major jurisdictions are parties to BITs with one another as there are

notable exceptions. Similarly, it should not be assumed that this might

only benefit investments in emerging markets or politically unstable

territories. While such jurisdictions are potentially more at risk of state

interference with investor rights, states with large developed economies

have also been subject to successful BIT claims.

Dispute resolution clause and disclosure

Dispute resolution clause and disclosure

The negotiation of an appropriate dispute resolution forum to resolve any

disputes that might arise out of the transaction is critical to the management of risk. A carefully drafted SPA needs to be capable of being enforced through a high-standard, quick and impartial dispute resolution mechanism resulting in a fair determination of any dispute, which can then be effectively enforced against the losing party wherever required.

![]() TEAM TIP:

TEAM TIP:

Where enforcement of a court judgment is likely to be difficult in jurisdictions where the counterparty has assets or where confidentiality is essential, arbitration is likely to be most appropriate.

Following the sale of a business, the buyer is likely to have most of the relevant information relating to the operations of that business, creating an asymmetry of information in favour of the buyer. In those circumstances, the buyer may want an arbitration clause to contain an express exclusion of any form of disclosure. This saves the buyer time and costs where it is less likely to need to rely on documents held by the seller and reinforces its advantageous position. The seller, on the other hand, having handed over substantial amounts of information relating to the operation of the business, is likely to want broad disclosure so as not to be disadvantaged should a dispute arise.

Restructuring the acquisition and saving important knowledge

Restructuring the acquisition and saving important knowledge

Often following an acquisition the business is restructured or people otherwise leave. Such people may hold key information about the business, including facts that might give rise to a claim against the seller, which might be lost.

![]() TEAM TIP:

TEAM TIP:

If a full post-completion audit cannot be completed prior to employee

departures, consider interviewing the employees prior to departure. At the very least ensure the target retains their emails and any company laptop or phone that might hold pre-acquisition data.

A buyer should ensure that if it intents to conduct a post-transaction

restructuring or merger, that this does not impact on the ability to make a claim against the seller. This might be done by way of succession language in the SPA.

Conversely, the seller may wish to include language providing that its liability will cease upon an onward transfer/disposal of the target in future.

Post-completion audit

Post-completion audit

While the processes for the preparation and closing of transactions – due

diligence, valuation and negotiating the purchase agreement – are carried out with great attention to detail and price adjustment for any issue discovered, often the focus post-completion is on integrating the business rather than ensuring the business is as warranted.

Many companies do not use standardized processes to uncover claims arising following corporate transactions. In many cases, the lack of targeted and standardized processes means that potential deficiencies in the acquired

company are only identified when pointed out by external third parties or

when obvious inconsistencies turn up. Deficiencies tend to be identified most

often in an ad hoc manner in connection with the preparation and auditing

of the annual financial statements. Such an approach means that claims

(and potential value) might be missed or picked up too late for a claim to be

brought under the purchase agreement.

![]() TEAM TIP:

TEAM TIP:

A buyer should consider conducting a detailed health-check of the business

following an acquisition (a form of post-acquisition due diligence) to ascertain the status of the target and to identify any issues or potential claims as early as possible. By conducting this review post-completion, (and provided it is carried out tactfully) the buyer has the benefit of being able to speak to all of the target’s staff frankly and without restriction and have access to all the target’s records. Issues that were highlighted as risk areas pre-acquisition should receive special attention as should any known matters that were subject to specific warranties or indemnities.

Companies that have carried out post-acquisition audits have not only found

accounting issues, but problems relating to breaches of competition law and

bribery legislation. By identifying these issues early, not only is the buyer able to bring a relevant claim against the seller within the prescribed time period, but it is also able to quickly bring an end to the practice post-acquisition which could be a key factor when dealing with the relevant competition and regulatory authorities.

Notification of claims

Notification of claims

A key risk area and an area where disputes frequently arise is the notification of claims. Under many governing laws the failure to strictly comply with such notification obligations both in terms of their timing and their form will result in the seller’s liability being excluded.

![]() TEAM TIP:

TEAM TIP:

Buyers should avoid any limitation period for the notification of claims that is triggered by awareness of an issue that might give rise to a claim, as opposed to a simple limitation period running from the date of completion. This is because the point at which a party becomes aware of an issue can be difficult to determine and lead to disputes as to when this has occurred. It also significantly increases the risk of claims inadvertently becoming time barred simply because information relating to a potential claim has not been passed on to the appropriate person within the buyer or acted upon promptly. It can also lead to notices of claims being given before all necessary information has been collected in order to meet a time limit triggered by awareness, but resulting in the actual notice being found to be invalid for lack of detail. If awareness of a claim cannot be excluded as the trigger for calculating the deadline for notification of the claim, the buyer should seek to mitigate this risk by limiting the category of people who need to be aware of the issue in question and being very specific as to the detail of knowledge they must have of the matter giving rise to a potential warranty claim in order for the buyer to be considered aware of the issue. The buyer should also restrict the effect of any failure to give timely notice to excluding the right to claim for any increase in losses caused by the delay.

Buyers should also seek to avoid legal proceedings having to be brought by

reference to the date of notification of any claim. At best it can result in piecemeal litigation (with different claims having to be commenced at different times) and at worst it can result in claims becoming barred whilst waiting for a de minimis threshold to be passed. Not having to commence proceedings by reference to the date of notification of a claim also avoids the risk of a notice of claim being given inadvertently, thereby unwittingly triggering the time limit for bringing a claim.

Immediately upon completion a buyer should diarise key dates on which limitation periods expire under the SPA. Before these deadlines the buyer should conduct a health check of business acquired, including speaking to the management team, to ascertain whether there are any issues that might trigger a claim under the SPA.

Dispute resolution Helping with M&A disputes

It is important for the success of any company or individual that the maximum value is derived from any M&A transaction. This can mean different things for sellers and buyers.

Sellers

Sellers wish to ensure that the maximum amount of consideration is obtained, which

might mean:

- Defending frivolous claims, and ensuring meritorious claims are settled promptly and

with the minimum of expense. - Preventing the buyer from seeking to engage in a post-transaction price adjustment, and ensuring that the buyer takes steps to ensure that any earn-outs are achieved.

Buyers

Buyers wish to ensure that they receive

the bargain they had entered into, which

might mean:

- Pursuing claims for breaches of warranty or misrepresentation which impact on the

correct value of the business. - Making appropriate completion account adjustments or protecting the goodwill of

the acquired business, including through the enforcement of restrictive covenants.

Often parties allow significant value from a M&A transaction to be leaked as a consequence of not managing the post-M&A process as well as the pre-Completion process. Examples include not conducting a thorough post-M&A review, including carrying out a health check of the business to ensure that the warranted or represented matters are as they should be and that the buyer and the seller are complying with their post-Completion obligations. Often warranty claims are raised out of time or so late that they are not adequately particularised and the resulting notification is invalid.